Migrating a B2B "Auto Pay" Program

Companies migrating to SAP often have daunting challenges to overcome in Accounts Receivable as part of the transition. You might have different divisions running on different ERP or AR systems, for example, and the migration will drive a unification effort. Whatever your specific case, driving improved AR process efficiency and predictability must be a core business goal of the migration.

A Fortune 100 company asked ArgonDigital to help them replace a critical financial system. Part of the project involved migrating their Business-to-Business automatic payment program (“Auto Pay”) from the legacy system to the new platform. Here is what we learned over 4 years working on a multi-phase project that delivered a complex, international Auto Pay solution. This robust, unified, solution manages hundreds of millions of dollars in yearly transactions and spans several international regions and partner bank integrations with distinct financial rulesets and compliance structures.

What Is B2B Auto Pay?

In an Auto Pay system, a customer allows a vendor or service provider to automatically debit a bank account each payment period for a specified amount. The amount due is typically tied to a regular invoicing cycle. Auto Pay is used when there is ongoing, regular commerce between a vendor and a buyer. Our experience has been in our clients’ B2B Auto Pay programs. (A Business-to-Consumer Auto Pay program will have different challenges compared to B2B and is outside the scope of this discussion.)

Common scenarios where B2B Auto Pay makes sense are financial contracts (loans, leases), subscription services, and regularly replenished components or hard goods supplies (raw materials, subcomponents, fasteners, etc.).

How Does B2B Auto Pay Work?

Implementing B2B Auto Pay requires the following systems and actors to work seamlessly together to perform well for customers and businesses:

1. A partner bank that will host your account and transact over the Automated Clearing House (ACH) network.

2. Your sales operations and finance teams will work together to enroll customers in Auto Pay.

3. Your Accounts Payable (AP) and Accounts Receivable (AR) teams will coordinate processes to generate and send invoices, and then to receive payments via the partner bank.

4. A set of AR systems sends an instruction to the partner bank to direct debit the customer’s account.

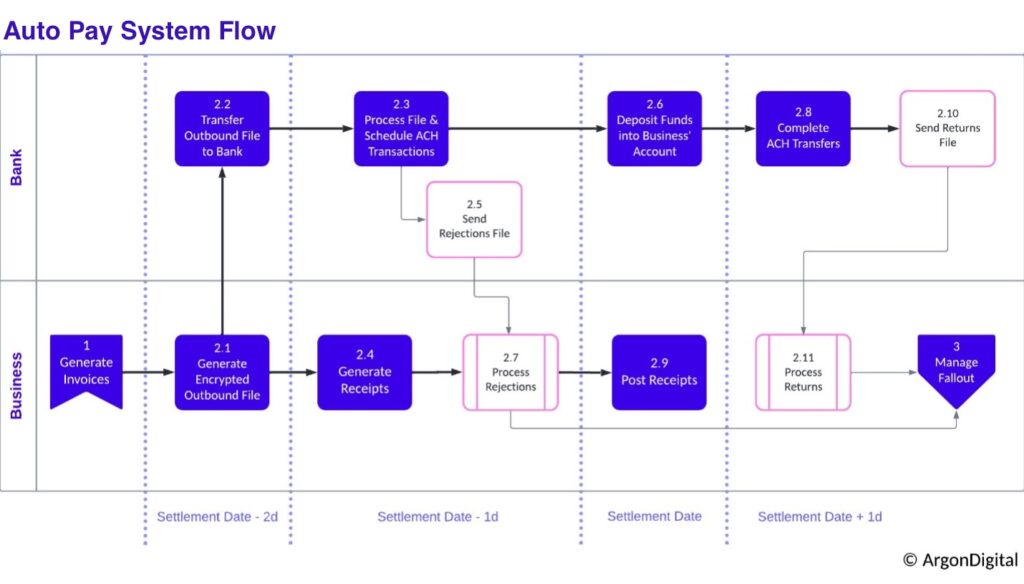

The overall process will be something like we portray in the system flow graphic below:

A few notes on the process:

1. This process starts when AP has sent an invoice (lower left) to the customer.

2. There are two “swim lanes” – one for the business, and one for the partner bank – where activities are running in parallel. The blue steps are the main actions while the pink shapes indicate conditional steps when there are issues.

3. The process works around a Settlement Date when the bank deposits funds into the business’ bank account. There are activities before and after that date, as indicated

4. In this case, the AR system sends an instruction to the partner bank via file. Some banks may have different means to securely transmit direct debit instructions.

5. There are three possible outcomes to the instruction your system must handle (your partner bank may use different terminology):

a. A successful direct debit

b. A rejected instruction (step 2.5), indicates that the bank cannot attempt the direct debit. An example is when your system sends an improperly formatted instruction, an invalid customer account number, etc.

c. A returned instruction (step 2.10), indicates that the bank attempted the direct debit, but did not complete successfully. An example is when the customer’s account balance was less than the debit amount (i.e., non-sufficient funds). ACH never debits other than the requested amount.

6. Typically, the bank credits the business’ account prior to completing the direct debit; obviously, any rejected debits reduce that deposit.

7. In the case of rejections or returns, you will need to have a process to correct issues:

a. Step 2.7 Process Rejection may involve a system or data issue to correct.

b. Step 2.11 Process Return involves reversing a receipt and requesting that the customer correct an account issue.

c. Either will involve “retrying” the debit.

8. Your AR cash reconciliation process should work around this sequence.

These basic elements of Auto Pay are relatively well established. The ACH standard describes how a bank expects to receive requests for a Direct Deposit on a customer’s behalf. It also lays out generally how the bank should conduct a transaction, and how the bank should communicate status. There are many advanced details to plan for and implementation must support these. See the Challenges section below for more details.

What Is The Business Value Of B2B Auto Pay?

An Auto Pay solution could be one of the most fruitful opportunities to reduce operations costs and prevent “revenue leakage” from your business. It can also enhance customer satisfaction over time.

The benefits to customers of a well-designed Auto Pay solution include:

- Reducing mistakes and confusion often resulting from a manual billing process.

- Helping customers to make timely and accurate payments, by eliminating instances of over- or under-payment. This can help to reduce their Accounts Payable workload.

- Since Auto Pay facilitates customers paying on time, it eliminates many “negative” vendor interactions such as assessment of late fees, incoming calls to ask for payment remittance, or outgoing calls to explain a confusing bill. These interactions often add stress to seller/buyer relationships and disrupt the partnering spirit of working together for better solutions.

Auto Pay solutions can do more than simply debit a customer’s account on time. The benefits to a business of a well-designed Auto Pay solution include:

- Radically reducing the manual effort necessary to track payments, process checks, and update cash application amounts for most customers. Associated manual “fallout” processes to manage underpayments, overpayments, late payments, non-payment, and misapplications of funds received can erode profitability and even threaten the health of a growing business.

- Simplifying Account Payable activity associated with late or erroneous payments.

- Scaling up the business without commensurate need for increased “back end” staffing.

- Since Auto Pay facilitates customers paying on time, it eliminates many “negative” customer interactions such as calling to ask for payment remittance or explaining an erroneous bill. These interactions often add stress to seller/buyer relationships and encourage customer ‘churn’.

Many businesses opt to automate their Accounts Receivable processes around Auto Pay. With very high confidence that each payment exactly matches the invoiced amount, AR can systematize the application of received funds to the correct receivables for the client, accurately and seamlessly applying cash according to business rules. This, in turn, allows AR teams to devote energy to higher-value activities, such as customizing payment scenarios for the most important customers or preventing delinquency that results in trouble contracts or the need for collections. Autopay also reduces common churn points around customer mistakes that result in delays and inconveniences.

Getting Started: What Are The Challenges In implementing B2B Auto Pay?

As noted above, the basic contours of Auto Pay are well established. However, a successful implementation requires defining and implementing every specific detail correctly. Challenges we have encountered include:

- A bank’s implementation of the ACH standard is tailored to its requirements, which often enable value-add features for their business clients. We have expended significant effort to align with those variations in process and data.

- Similarly, an AR system’s “out of the box” ACH support may not work with the bank’s implementation, so it may be necessary to customize the system.

- Auto Pay involves exchanging customer bank account information with an external partner bank; data security at every step must be absolutely assured.

- There is an extraordinarily high standard of performance in executing an AutoPay feature:

- Your system must never initiate duplicate Direct Debit requests or miss a valid Direct Debit request.

- Direct Debit requests must exactly equal the invoice which has been sent to the customer.

- The cash applications and reconciliation processes must account for every possible permutation in results.

Poor design, defects in features, or mistakes in process implementation have the potential to inflict severe financial harm on the business. Implementation and testing must meet exacting standards before launching with customers.

Why Work With ArgonDigital On B2B Auto Pay?

ArgonDigital brings years of experience across multiple geographic regions to help you with your Auto Pay implementation. Our strengths include business requirements, technical implementation, as well as Product and Program Management to deliver successful solutions. Our approach begins with eliciting and documenting a comprehensive set of requirements for Auto Pay. We use visual modeling to identify all use cases (inclusive of edge cases and fallout scenarios), which becomes increasingly important in proportion to the complexity of the solution space. Our solution development team has decades of experience designing, developing, and maintaining solutions.